It is refreshing to see top academics questioning some of the assumptions that economists have been using in their models. Krugman, Brad DeLong and many others are opening a methodological debate about what constitute an acceptable economic model and how to validate its predictions. The role of micro foundations, the existence of a natural state towards the economy gravitates,... are all very interesting debates that tend to be ignored (or assumed away) in academic research.

I would like to go further and add a few items to their list that I wished could become part of the mainstream modeling in economics. In random order:

1. The business cycle is not symmetric. Most macroeconomic models start with the idea that fluctuations are caused by a succession of events that are both positive and negative (on average they are equal to zero). Not only this is a wrong representation of economic shocks but is also leads to the perception that stabilization policy cannot do much. Interestingly, it was Milton Friedman who put forward the "plucking" model of business cycles as an alternative to the notion that fluctuations are symmetric. In Friedman's model output can only be below potential or maximum. If we were to rely on asymmetric models of the business cycle, our views on potential output and the natural rate of unemployment would be radically different. We would not be rewriting history to claim that in 2007 GDP was above potential in most OECD economies and we would not be arguing that the natural unemployment rate in Souther Europe is very close to its actual.

2. As much as the NBER methodology emphasizes the notion of recessions (which, by the way, is asymmetric in nature), most academic research is produced around models where small and frequent shocks drive economic fluctuations, as opposed to large and infrequent events. The disconnect comes probably from the fact that it is so much easier to write models with small and frequent shocks than having to define a (stochastic?) process for large events. It gets even worse if one thinks that recessions are caused by the dynamics generated during expansions. Most economic models rely on unexpected events to generate crisis, and not on the internal dynamics that precede the crisis.

[A little bit of self-promotion: my paper with Ilian Mihov on the shape and length of recoveries presents some evidence in favor of these two hypothesis.]

3. There has to be more than price rigidity. Keynesian models rely on price rigidity to explain business cycles and why demand matters. There is plenty of evidence that price rigidities are important and they help us understand some of the features of the business cycle. But there must be more than that. There are other frictions in the real economy that produce a slow adjustment and are responsible for the persistence of business cycles. They might not be easy to measure or model, they might be different across different economies but it is difficult to imagine that an adjustment of prices and wages to its optimal level would automatically restore full employment. Larry Summers referred to these frictions in his recent IMF conference speech although he did not elaborate on them.

4. The notion that co-ordination across economic agents matters to explain the dynamics of business cycles receives very limited attention in academic research. It some times appear in our economic policy debate (e.g. Olivier Blanchard (at the IMF) has referred to multiple equilibria as a way to explain the sovereign-debt crisis in Europe) but it does nor receive the credibility it deserves in academia.

I am aware that they are plenty of papers that deal with these four issues, some of them published in the best academic journals. But most of these papers are not mainstream. Most economists are sympathetic to these assumption but avoid writing papers using them because they are afraid they will be told that their assumptions are ad-hoc and that the model does not have enough micro foundations (for the best criticism of this argument, read the latest post of Simon Wren-Lewis). Time for a change?

Antonio Fatás

Monday, December 16, 2013

Tuesday, December 10, 2013

Debt and secular stagnation

In a recent post Paul Krugman refers to the potential link between rising levels of debt prior to the 2008 crisis and the current discussion on secular stagnation. The argument can be illustrated by the chart below (borrowed from Krugman's post).

Quoting from Krugman's post:

"Debt was rising by around 2 percent of GDP annually; that's not going to happen in the future, which a naive calculation suggests a reduction in demand, other things equal, of around 2 percent of GDP"

In summary, increasing debt ratios area unsustainable and the adjustment can have a negative effect on growth. The argument is probably right but when it comes to assessing the real impact on growth I think we need to do a more careful analysis before reaching that conclusion.

Here is where I think the reading of the previous chart becomes more complicated: Why was debt going up? For some this is simply a reflection of excessive spending that directly feeds into demand. The fact that it is excessive leads to the need to reverse the trend in the years that follow and, using the same logic but now going back, it will lead to a reduction in demand. But to reach that conclusion we first need to do a more careful analysis of the balance sheet of US households by looking not only at their liabilities but also at their assets. Below is a chart of total assets (blue line) and just financial assets (red line) during the same period of time (and both measured as % of GDP).

We also observe an upward trend. How do these two trends (assets and liabilities) compare? We can measure it by looking at the difference between assets and liabilities = net wealth of US households (as % of GDP).

What we see is also an upward trend with large volatility around the last two recessions. An upward trend means that asset values are growing faster than debt. Today's net wealth is below the peak of 2005-2006 but it is above the level of any other year in the sample. With this new perspective it is more difficult to conclude that debt is still high or that it cannot grow from current levels.

What I find more interesting (and intriguing) is that rising debt (as a % of GDP) at the same time as asset values increase (even faster) is not the exception but the norm when one looks at a larger sample.

Below is the evolution of Household Debt (blue, right axis) and Net Worth (red, left axis), both as % of GDP during the 1975-1995 period. So I am excluding the last two asset price bubbles to look at a more "normal" period. We still see rising trends for both series. So debt ratios were increasing fast but asset values were growing at an even faster rate, so the net worth kept going up through those 20 years.

What these charts suggest is that the analysis of debt is a complex one and it requires a careful look at both sides of the balance sheet. And unless I am missing some relevant academic research, we do not have a good framework to think about these trends. And things can get a lot more complicated if we start adding other issues, such as the distribution of holdings of assets and liabilities. It could be that the households that are holding the assets are not be the same as the ones holding the debt, and this can change the way we think about the implications of these trends.

Antonio Fatás

Thursday, December 5, 2013

Battle lost: austerity won.

It has been surprising to see how over the last five years some have been holding to their economic theories even if the facts kept proving them wrong (Yyperinflation? Confidence and austerity?). At the end, it seems that ideology dominates much of the macroeconomic analysis we see these days. But what is more surprising is how broad this phenomenon is and how the general economic commentary that one reads in the press cannot move away from those theories either.

One statement that will not go away is the constant reference to "printing money" which is not only incorrect from a factual point of view (most of the increase in the monetary base corresponds to reserves not to bank notes being printed) but also misleading when it comes to the understanding of the role of central banks. Even those who support central bank actions during the crisis have to add a sentence at the end to warn us about the danger of so much liquidity.

And austerity, as much as the data has disproven the claim that it would be through reduction in government spending and increased confidence that advanced economies will return to healthy growth rates, it does not seem to lose its appeal either. As an example, here is a CNBC article that provides a long list of arguments of why austerity is winning the war. The arguments: the UK is finally growing, Spain's GDP is not falling anymore and even in Greece we now start seeing the possibility of positive growth. And where is this coming from? From the austerity that these wise governments have implemented over the last year. This is, of course, a misleading analysis of the data. It is still the case that countries where austerity was the strongest have seen the lowest growth rates (and the largest increase in debt). The only reason why these three countries are either returning to growth or not collapsing anymore is that after such a deep crisis, growth must return at some point. Yes, even without any policy actions to support growth, economies recover. But they do so slowly and they will never return to where they should have been. And just to get the facts straight, in these three countries, governments have stopped being a large drag in the economy. When you reduce government spending growth suffers. Once government has stabilized at a low level it does not become a drag on growth.

The last five years have provided an incredible macroeconomic experiments to learn about the effects of monetary and fiscal policy to stabilize cycles. But it seems that this crisis will be wasted, not so much in terms of implementing reforms but in terms of our ability to use data to improve our understanding of macroeconomics.

Antonio Fatás

One statement that will not go away is the constant reference to "printing money" which is not only incorrect from a factual point of view (most of the increase in the monetary base corresponds to reserves not to bank notes being printed) but also misleading when it comes to the understanding of the role of central banks. Even those who support central bank actions during the crisis have to add a sentence at the end to warn us about the danger of so much liquidity.

And austerity, as much as the data has disproven the claim that it would be through reduction in government spending and increased confidence that advanced economies will return to healthy growth rates, it does not seem to lose its appeal either. As an example, here is a CNBC article that provides a long list of arguments of why austerity is winning the war. The arguments: the UK is finally growing, Spain's GDP is not falling anymore and even in Greece we now start seeing the possibility of positive growth. And where is this coming from? From the austerity that these wise governments have implemented over the last year. This is, of course, a misleading analysis of the data. It is still the case that countries where austerity was the strongest have seen the lowest growth rates (and the largest increase in debt). The only reason why these three countries are either returning to growth or not collapsing anymore is that after such a deep crisis, growth must return at some point. Yes, even without any policy actions to support growth, economies recover. But they do so slowly and they will never return to where they should have been. And just to get the facts straight, in these three countries, governments have stopped being a large drag in the economy. When you reduce government spending growth suffers. Once government has stabilized at a low level it does not become a drag on growth.

The last five years have provided an incredible macroeconomic experiments to learn about the effects of monetary and fiscal policy to stabilize cycles. But it seems that this crisis will be wasted, not so much in terms of implementing reforms but in terms of our ability to use data to improve our understanding of macroeconomics.

Antonio Fatás

Monday, December 2, 2013

Where did the saving glut go?

I have written before about the investment dearth that took place in advanced economies at the same time that we witnessed a global saving glut as illustrated in the chart below. In particular, the 2002-2007 expansion saw lower investment rates than any of the previous two expansions.

Antonio Fatás

P.S. All data used to produce the charts above comes from the IMF World Economic Outlook. Individual country data has been aggregated using PPP GDP weights (using market exchange rates GDP weights provides very similar insights).

If one thinks about a simple demand/supply framework using the saving (supply) and investment (demand) curves, this means that the investment curve for these countries must have shifted inwards at the same time that world interest rates were coming down.

But what about emerging markets? Emerging markets' investment did not fall during the last 10 years, to the contrary it accelerated very fast after 2000.

This is more what one would expect as a reaction to the global saving glut. The additional saving must be going somewhere (saving must equal investment in the world). As interest rates are coming down, emerging markets engage in more investment (whether this is simply a move along a downward-slopping investment curve or a shift of the investment opportunities for any given level of interest rates is impossible to tell from this simple analysis).

We can also look at the world as whole

Starting in the year 2000 we see a trend towards higher investment driven by emerging markets.

In equilibrium, both saving and investment have to move by the same amount (at the global level) so how do we know that this is a saving glut and not an increase in investment opportunities? The fact that interest rates were declining during these years means that these changes were dominated by an outward shift in the saving curve (if it had been investment shifting we would have seen interest rates increased). The resulting lower interest rates led to higher investment in emerging markets, as expected, but they did not foster any additional investment in advanced economies signaling that there has been a decline in investment opportunities in these countries. Whether this is a sign of a structural weakness that affects the inability of advanced economies to keep innovating at the same rate or purely a reflection of other, possibly cyclical, factors remains an open question.

Antonio Fatás

P.S. All data used to produce the charts above comes from the IMF World Economic Outlook. Individual country data has been aggregated using PPP GDP weights (using market exchange rates GDP weights provides very similar insights).

Sunday, November 24, 2013

Euro workers: no systemic risk

In his last press conference Mario Draghi said that the ECB was ready for negative deposit rates if necessary. His comments led to several European bankers rejecting this as a possibility (here and here). The comments of the Deutsche Bank and Commerzbank CEOs reflect on either their ignorance of how monetary policy works or their fighting against an ECB action that could make their lives harder (and their profits lower).

Martin Blessing from Commerzbank argues that "too much cheap credit could lead to future crises" and he concludes that he does not know "how too much cheap liquidity can solve a problem that was created by too much cheap liquidity." This argument has now been wrongly used for 5 years, I thought that by now we would have learned that this is the wrong analogy.

Fischen from Deutsche Bank complains that setting negative interest rates on deposits at the ECB would be like "penalizing banks". And this "will later be felt in a painful manner so that's what I've been warning about" (a threat?). This is the usual argument that banks are so important that you cannot do anything that annoys them. But what if negative interest rates are the right equilibrium value? In what way are we penalizing banks? Banks can go and invest their funds somewhere else if they find that this is not a competitive rate. In addition, it is not uncommon to have these CEOs arguing that what the Euro zone needs (in particular countries in the periphery) is a large reduction in wages. I guess this is fine. "Penalizing" workers is ok because they do not pose any systemic risk to the economy as a whole.

Antonio Fatás

Martin Blessing from Commerzbank argues that "too much cheap credit could lead to future crises" and he concludes that he does not know "how too much cheap liquidity can solve a problem that was created by too much cheap liquidity." This argument has now been wrongly used for 5 years, I thought that by now we would have learned that this is the wrong analogy.

Fischen from Deutsche Bank complains that setting negative interest rates on deposits at the ECB would be like "penalizing banks". And this "will later be felt in a painful manner so that's what I've been warning about" (a threat?). This is the usual argument that banks are so important that you cannot do anything that annoys them. But what if negative interest rates are the right equilibrium value? In what way are we penalizing banks? Banks can go and invest their funds somewhere else if they find that this is not a competitive rate. In addition, it is not uncommon to have these CEOs arguing that what the Euro zone needs (in particular countries in the periphery) is a large reduction in wages. I guess this is fine. "Penalizing" workers is ok because they do not pose any systemic risk to the economy as a whole.

Antonio Fatás

Wednesday, November 20, 2013

Saving glut or investment dearth?

Martin Wolf at the Financial Times argues that the future of the world economy, in particular that of advanced economies, looks sluggish because investment rates have displayed a downward trend over recent years, even before the financial crisis started. I made similar points in my blog post yesterday, let me add some evidence to that story.

It is a fact that since the mid 1990s interest rates in the world started a downward trend. This trend was explained by Ben Bernanke in his March 2005 speech

“To be more specific, I will argue that over the past decade a combination of diverse forces has created a significant increase in the global supply of saving--a global saving glut--which helps to explain the relatively low level of long-term real interest rates in the world today”

This can easily be represented in a standard demand and supply chart for the global market for funds where the saving glut is simply a shift of the saving (supply) curve to the right.

What was interesting about the saving glut hypothesis is that it not only explained the decrease in interest rates but it was also able to account for the growth in global imbalances. One simple way to represent that is to separate the world in two blocks: those whose saving increased and the rest of the world. We can use again a simple demand and supply chart to represent this two group of countries: we represent the countries whose saving was increasing on the left hand side and the rest of the world on the right hand side to get the following picture:

This shows that we should expect the countries that increase their saving to display a growing current account surplus and the countries where the two curves are not shifting to display a growing current account deficit. This simple framework matches well the data during those years. Current account surplus in countries such as Germany, Japan, Oil producing countries, China and other emerging markets in Asia increased while deficits in countries such as the US and Greece, Spain, Portugal, Ireland, the UK increased as well. Here is the data (from the IMF World Economic Outlook):

But in this story there were some predictions that were never tested. In particular, as interest rates fell, investment should have increased globally. If you look at the saving and investment curves above, investment should have increased both in countries where the supply of saving was shifting as well as in the other countries. Unless we believe that investment rates do not depend on the interest rates we should have seen a generalized increased in investment around the world. Did we see that? No. In fact in advanced economies (including the US, as I showed yesterday) we have seen the opposite. Below is a chart that I have constructed using data from the IMF (World Economic Outlook database). I have calculated the aggregate investment rate (as % of GDP) for all advanced economies using the GDP share of each of these countries as weights [using PPP adjusted weights makes no difference for these countries].

There is a clear downward trend in the data. Even if we ignore the post-2008 data. the expansion in the 2000s was weaker that that of the 90s or the 80s. And remember that we expected exactly the opposite. The only way to make this last chart compatible with the saving glut story is to argue that at the same time that the saving curve was shifting to the right in some countries, the investment curve was also shifting (this time inwards) in other countries.

The shift of the investment curve would also help explain the lower interest rate during the decade. But in addition it would explain why growth rates (and labor market performance) remained weak during the expansion of the 2000s in some advanced economies. And given what we have seen so far during the current expansion it might be a source of additional pessimism about the coming years.

Antonio Fatás

It is a fact that since the mid 1990s interest rates in the world started a downward trend. This trend was explained by Ben Bernanke in his March 2005 speech

“To be more specific, I will argue that over the past decade a combination of diverse forces has created a significant increase in the global supply of saving--a global saving glut--which helps to explain the relatively low level of long-term real interest rates in the world today”

This can easily be represented in a standard demand and supply chart for the global market for funds where the saving glut is simply a shift of the saving (supply) curve to the right.

What was interesting about the saving glut hypothesis is that it not only explained the decrease in interest rates but it was also able to account for the growth in global imbalances. One simple way to represent that is to separate the world in two blocks: those whose saving increased and the rest of the world. We can use again a simple demand and supply chart to represent this two group of countries: we represent the countries whose saving was increasing on the left hand side and the rest of the world on the right hand side to get the following picture:

This shows that we should expect the countries that increase their saving to display a growing current account surplus and the countries where the two curves are not shifting to display a growing current account deficit. This simple framework matches well the data during those years. Current account surplus in countries such as Germany, Japan, Oil producing countries, China and other emerging markets in Asia increased while deficits in countries such as the US and Greece, Spain, Portugal, Ireland, the UK increased as well. Here is the data (from the IMF World Economic Outlook):

But in this story there were some predictions that were never tested. In particular, as interest rates fell, investment should have increased globally. If you look at the saving and investment curves above, investment should have increased both in countries where the supply of saving was shifting as well as in the other countries. Unless we believe that investment rates do not depend on the interest rates we should have seen a generalized increased in investment around the world. Did we see that? No. In fact in advanced economies (including the US, as I showed yesterday) we have seen the opposite. Below is a chart that I have constructed using data from the IMF (World Economic Outlook database). I have calculated the aggregate investment rate (as % of GDP) for all advanced economies using the GDP share of each of these countries as weights [using PPP adjusted weights makes no difference for these countries].

There is a clear downward trend in the data. Even if we ignore the post-2008 data. the expansion in the 2000s was weaker that that of the 90s or the 80s. And remember that we expected exactly the opposite. The only way to make this last chart compatible with the saving glut story is to argue that at the same time that the saving curve was shifting to the right in some countries, the investment curve was also shifting (this time inwards) in other countries.

The shift of the investment curve would also help explain the lower interest rate during the decade. But in addition it would explain why growth rates (and labor market performance) remained weak during the expansion of the 2000s in some advanced economies. And given what we have seen so far during the current expansion it might be a source of additional pessimism about the coming years.

Antonio Fatás

Tuesday, November 19, 2013

Bubbles, interest rates and full employment.

The presentation of Larry Summers at a recent IMF conference has generated a good amount of comments. While some of what he said was not completely new, the way he put together some of these ideas to present a fairly pessimistic view of the state of the US economy has led to a debate around the possibility of secular stagnation (see Krugman). Secular stagnation refers to the fact that some of the output losses during the crisis become permanent, the economy does not ever return to the previous trend.

But there was something else that Larry Summers discussed that I also find interesting: he referred to the fact that in previous expansions the US economy barely managed to reach full employment despite the existence of strong bubbles and excesses. This also leads to a pessimistic view of the recent years and not so much because of what happened after 2008 but what happened before 2008.

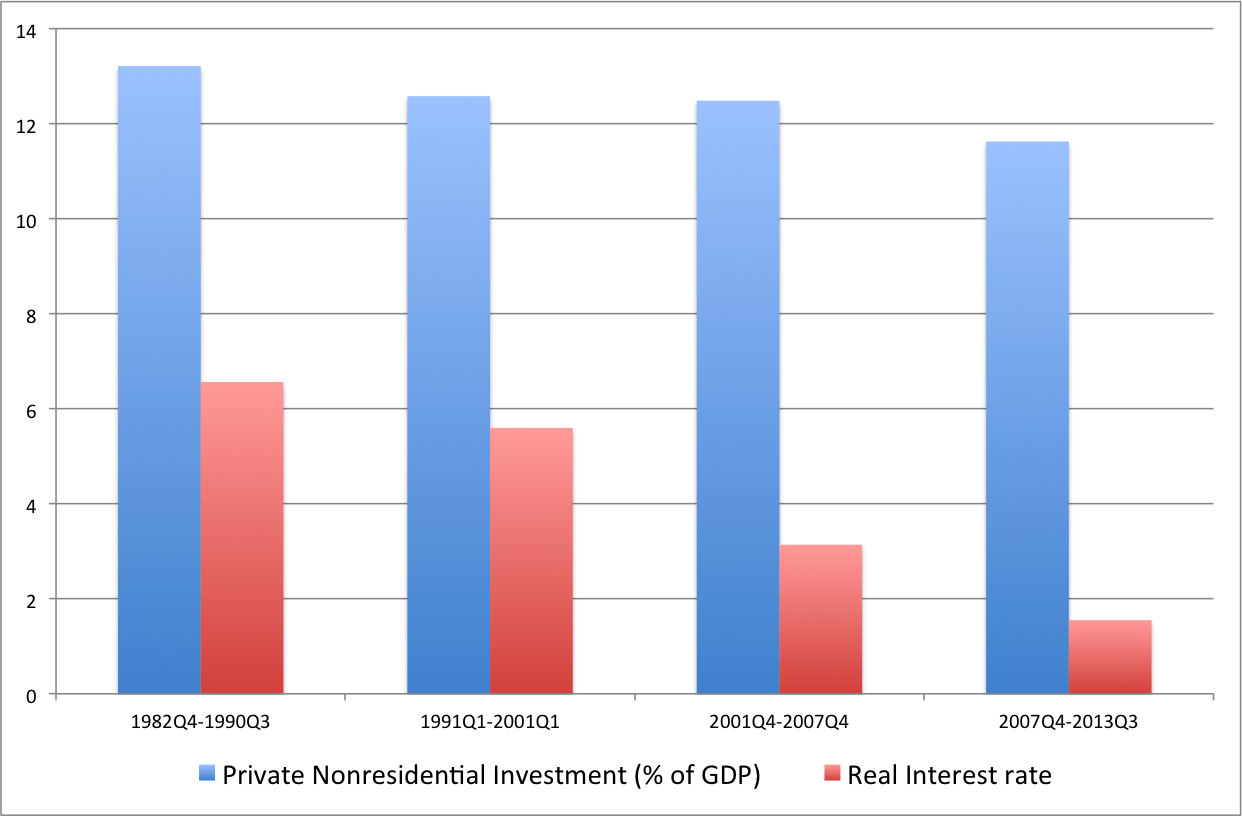

Here is some data and a story to make you share that pessimism: it is a fact that global real interest rates during the last expansion (2001-2007) were very low by historical standards. The main candidate to explain low real interest rates is the saving glut that Ben Bernanke referred to in his 2005 speech to describe the increase in the pool of global saving coming from Asia, Germany, Japan and oil producing countries. As saving increase, the world interest rate fell. In other countries (such as the US and some European countries), this led to an increase in spending and borrowing that resulted in an increase in global imbalances.

But if what we saw in these years was an increase in the pool of saving that drove down interest rates we should expect investment to increase (as supply shifts we move along a downward slopping demand curve to find the new equilibrium price). And if investment increases we should expect an increase in growth rates. But none of this happened. In fact, investment not only did not go up but it was lower than what it had been in previous expansions as shown in the chart below (data is for the US economy).

When we compare the last four expansions in the US economy we can see that while the real interest rate kept going down (especially in the 2001-2007 expansion), investment rates remained flat or even declined. I have included the current expansion in the chart although is not comparable to the others as it has not finished yet.

What happened to investment? Why didn't it go up as real interest rates fell and the pool of saving was increasing? I am not sure we have an answer to these questions but what the data suggests is that we are not just facing the negative consequences of a deep recession, we should also have some concerns about the strength of the recovery based on the weakness of investment in the previous expansion (once we take into account the low level of interest rates).

Antonio Fatás

Sunday, November 17, 2013

Europe: lack of reforms or austerity?

In a recent Vox article, Lorenzo Bini Smaghi raises some questions about the argument that austerity is the main reason why European countries' growth rates have been so low since 2008. To be fair, he is open to the idea that austerity has done some damage but he suggests that structural issues are also responsible for what we have seen in Southern European countries.

His main argument can be summarized by a set of charts where growth during the 2008-2012 period is shown to be negatively correlated to measures of competitiveness. For example, comparing growth during the crisis with the competitiveness index produced by the World Economic Forum, one gets the following correlation:

So the argument is that the low growth performance of Southern Europe (and Ireland) during the crisis is related to their structural problems.

I will not disagrees with the statement that some of those countries have structural weaknesses that can constraint their growth rates. But I find that the chart above does not provide much insights on how much growth reforms could deliver or the extent to which lack of reforms are behind the depth of the recession in these countries.

My concern is the use of only 4 years to assess the effects of competitiveness. If structural weaknesses matter so much, they should affect growth in the long term (not just during crisis). If one compares the evolution of GDP growth since 1994 among some of these countries, the picture looks very different (click on the image for a larger version)

For every year in the period 1994-2009 (without exception) growth in Spain or Greece was higher than in Germany (and without the exception of 1998 this is also true when compared to Austria). It is only during the years 2010-2012 where Austria and Germany display faster growth rates than Spain and Greece. And it is in those years that austerity was the strongest. So what we have is countries where the amplitude of the business cycle is much larger. They did better during the good years and now they are doing worse, which is not a big surprise (e.g. the volatility of emerging markets tends to be larger than that of advanced economies). And given what happened in those years in terms of austerity and the fact that financial markets remain dysfunctional it is even less of a surprise. No doubt that structural weaknesses exist in these countries but their connection to growth is a complex one and cannot simply be assessed by looking at the last three years.

Antonio Fatás

His main argument can be summarized by a set of charts where growth during the 2008-2012 period is shown to be negatively correlated to measures of competitiveness. For example, comparing growth during the crisis with the competitiveness index produced by the World Economic Forum, one gets the following correlation:

So the argument is that the low growth performance of Southern Europe (and Ireland) during the crisis is related to their structural problems.

I will not disagrees with the statement that some of those countries have structural weaknesses that can constraint their growth rates. But I find that the chart above does not provide much insights on how much growth reforms could deliver or the extent to which lack of reforms are behind the depth of the recession in these countries.

My concern is the use of only 4 years to assess the effects of competitiveness. If structural weaknesses matter so much, they should affect growth in the long term (not just during crisis). If one compares the evolution of GDP growth since 1994 among some of these countries, the picture looks very different (click on the image for a larger version)

For every year in the period 1994-2009 (without exception) growth in Spain or Greece was higher than in Germany (and without the exception of 1998 this is also true when compared to Austria). It is only during the years 2010-2012 where Austria and Germany display faster growth rates than Spain and Greece. And it is in those years that austerity was the strongest. So what we have is countries where the amplitude of the business cycle is much larger. They did better during the good years and now they are doing worse, which is not a big surprise (e.g. the volatility of emerging markets tends to be larger than that of advanced economies). And given what happened in those years in terms of austerity and the fact that financial markets remain dysfunctional it is even less of a surprise. No doubt that structural weaknesses exist in these countries but their connection to growth is a complex one and cannot simply be assessed by looking at the last three years.

Antonio Fatás

Wednesday, November 13, 2013

Why Sinn was wrong to write this FT article

When I teach these days about the negative performance of the Euro economies over the last six years I always get asked about how policy makers could get it so wrong. The answer can be found in the article that Hans-Werner Sinn published today in the Financial Times (Why Draghi was wrong to cut interest rates). It is hard to know where to start commenting on the article. It is not only inconsistent but also full of arguments that go against any economic logic and misleading use of partial data.

Interestingly, the article starts with the argument that given that inflation in the Euro area is below its target and falling (down to 0.7% in October), it seems that "last week's interest rate cut is understandable". Correct. That's the only reasonable paragraph of the article as the next one opens with the sentence:

"However, deflation in parts of a currency union is not the same as deflation of a union as a whole, because its internal effects on competitiveness cannot be compensated for by exchange rate adjustment.".

Let me start with the first part of the sentence. It is interesting proposition to argue that the ECB should not manage just average inflation (and growth?) but also try to manage these variables at the regional variable. This is not the mandate of the ECB. And what is exactly what Hans-Werner Sinn proposes, that the ECB tries to keep inflation in any region (country?) of the Euro area below 2%? This will imply overall deflation in the Euro area.

The second part of the sentence is even worse. If it is true that we need a realignment of relative prices within the Euro area, you will NOT get it by keeping inflation low. The article argues that the "printing presses" from Souther Europe have slowed down the realignment of the relative prices of goods needed for improving competitiveness. Wrong. There is plenty of evidence that prices and wages exhibit downward nominal rigidity and that it is much easier to allow changes in relative prices when inflation is positive. It is the low inflation level of the Euro area that is limiting the adjustment in relative prices (Krugman makes this point today in his blog).

The article also argues that the ECB policies have kept the value of the Euro down and this is one of the reasons why the German economy is running a current account surplus (not sure which chart he is looking at to argue that the value of the Euro is low...).

Antonio Fatás

Interestingly, the article starts with the argument that given that inflation in the Euro area is below its target and falling (down to 0.7% in October), it seems that "last week's interest rate cut is understandable". Correct. That's the only reasonable paragraph of the article as the next one opens with the sentence:

"However, deflation in parts of a currency union is not the same as deflation of a union as a whole, because its internal effects on competitiveness cannot be compensated for by exchange rate adjustment.".

Let me start with the first part of the sentence. It is interesting proposition to argue that the ECB should not manage just average inflation (and growth?) but also try to manage these variables at the regional variable. This is not the mandate of the ECB. And what is exactly what Hans-Werner Sinn proposes, that the ECB tries to keep inflation in any region (country?) of the Euro area below 2%? This will imply overall deflation in the Euro area.

The second part of the sentence is even worse. If it is true that we need a realignment of relative prices within the Euro area, you will NOT get it by keeping inflation low. The article argues that the "printing presses" from Souther Europe have slowed down the realignment of the relative prices of goods needed for improving competitiveness. Wrong. There is plenty of evidence that prices and wages exhibit downward nominal rigidity and that it is much easier to allow changes in relative prices when inflation is positive. It is the low inflation level of the Euro area that is limiting the adjustment in relative prices (Krugman makes this point today in his blog).

The article also argues that the ECB policies have kept the value of the Euro down and this is one of the reasons why the German economy is running a current account surplus (not sure which chart he is looking at to argue that the value of the Euro is low...).

Antonio Fatás

Thursday, October 31, 2013

Party like it's 1995?

For some it is clear that the all-time record levels in the stock market are supported by loose monetary and the day policy starts changing, stock markets will suffer a sharp drop. While I also worry about the tendency of stock markets and investors to be overoptimistic, I am less concerned by the fact that we are hitting all-time record levels. First, we keep forgetting that we are talking about nominal variables and they will keep setting record levels as long as inflation remains positive. But I am also less worried because tightening of monetary policy normally happens when growth is picking up so the stock market will have to decide if they like more faster growth than higher interest rates. And the reaction might surprise some.

Whatever else might be wrong with the U.S. economy, the stock and bond markets of Wall Street are thriving on the strength of falling interest rates. Sluggish job growth, subdued consumer spending and worries about how the nation will fare in an increasingly competitive world have not stopped the steady advance of stock prices to record highs. Fort Worth Star-Telegram. August 26, 1993.

Fed Fears a Market Bubble If It Lowers Interest Rates. New York Times, September 16, 1993.

Stocks climb to a record Surge in bonds, lower interest rates are behind it. It was the Dow's fourth record close this month. The Associated Press, August 20, 1993.

Jump in interest rates sends shiver through bull market. The bull market that carried blue chip stocks to record highs last week may be running out of steam - and the next move could be nasty as small investors try to get out of the market, analysts say. Indeed, there is concern on Wall Street that the record flow of money into stock and bond mutual funds has created a potentially dangerous situation.

Signs of market fragility reappeared Friday when a jump in interest rates on the bond market triggered a selloff in stocks. The Washington Post, May 30, 1993.

A lot of these headlines look identical to the ones we read today. What happened in that historical episode can be seen in the chart below where I compare the evolution of the interest rate (Fed Funds Rate) with the Dow Jones Index (click for a larger image).

As interest rates started increasing towards the end of 1993 the stock market moved sideways (and it fell during some of the quarters). But as of the second quarter of 1994 the stock market recovered, paused towards the end of the year and then started a bull run that would continue for several years. What is interesting is that during 1995 monetary conditions continued to get tighter but the stock market kept booming. [I stopped my chart in 1996 but in the four years that followed the stock market doubled again]

I have no reason to expect the same behavior in the stock market this time (and given what happened after 2000, it might not be a desirable outcome), but these years serve as an illustration of how markets reacted positively to a significant reversal in monetary policy. Initially there was uncertainty and weakness in the stock market but it was later followed by strong optimism even if interest rates kept going up.

Antonio Fatás

A historical example that I have mentioned earlier and that I find interesting is the period 1993-1996. In 1993 the recovery from the previous recession was slowly taking shape and the stock market was going up and, yes, setting all-time records. What did the newspaper headlines say at the time and also in anticipation of a future when monetary policy was about to get tighter? A quick search in Google reveals the following headlines:

Whatever else might be wrong with the U.S. economy, the stock and bond markets of Wall Street are thriving on the strength of falling interest rates. Sluggish job growth, subdued consumer spending and worries about how the nation will fare in an increasingly competitive world have not stopped the steady advance of stock prices to record highs. Fort Worth Star-Telegram. August 26, 1993.

Fed Fears a Market Bubble If It Lowers Interest Rates. New York Times, September 16, 1993.

Stocks climb to a record Surge in bonds, lower interest rates are behind it. It was the Dow's fourth record close this month. The Associated Press, August 20, 1993.

Jump in interest rates sends shiver through bull market. The bull market that carried blue chip stocks to record highs last week may be running out of steam - and the next move could be nasty as small investors try to get out of the market, analysts say. Indeed, there is concern on Wall Street that the record flow of money into stock and bond mutual funds has created a potentially dangerous situation.

Signs of market fragility reappeared Friday when a jump in interest rates on the bond market triggered a selloff in stocks. The Washington Post, May 30, 1993.

A lot of these headlines look identical to the ones we read today. What happened in that historical episode can be seen in the chart below where I compare the evolution of the interest rate (Fed Funds Rate) with the Dow Jones Index (click for a larger image).

As interest rates started increasing towards the end of 1993 the stock market moved sideways (and it fell during some of the quarters). But as of the second quarter of 1994 the stock market recovered, paused towards the end of the year and then started a bull run that would continue for several years. What is interesting is that during 1995 monetary conditions continued to get tighter but the stock market kept booming. [I stopped my chart in 1996 but in the four years that followed the stock market doubled again]

I have no reason to expect the same behavior in the stock market this time (and given what happened after 2000, it might not be a desirable outcome), but these years serve as an illustration of how markets reacted positively to a significant reversal in monetary policy. Initially there was uncertainty and weakness in the stock market but it was later followed by strong optimism even if interest rates kept going up.

Antonio Fatás

Sunday, October 27, 2013

Sudden stops and exchange rates (again)

I did not realize that some of my earlier posts on sudden stops and the Euro area would be so controversial, I thought I was making a simple point. And this time those who disagree with me are the ones that I always agree with so it makes you think even harder about whether the argument that I was making are right!

Brad DeLong wrote a post yesterday to show that sudden (capital) stops should not be a concern for countries that have their own currencies. Let me start with all the arguments where I do not have any disagreement:

- Taking about the possibility of a sudden stop in the UK or the US makes no sense. I agree. The comparison that some establish to argue that the "US is the next Greece" is idiotic.

- Countries with fixed exchange rates that have accumulated a large amount of debt denominated in foreign currency are more likely to be exposed to crisis caused by sudden stops. Correct.

Where we disagree is on whether sudden stops are relevant to other countries with flexible exchange rates. My argument was that in cases where countries have been running large current account deficit for years, a sudden stop of capital could be contractionary (i.e. cause a crisis). Brad DeLong is more optimistic and argues (using the IS-LM model) that, on the contrary, a sudden stop will be expansionary because the exchange rate depreciation will boost exports. The argument is correct within the context of that model but I think that the model is missing several ingredients.There is no one real interest rate in financial markets. You might fix this by adding some risk premium to the model (e.g. the interest rate in the investment equation has an extra term). As long as that extra term is constant it will look as if you can still generate an expansion by controlling the real interest rate but I think that in some cases markets just fail to even provide a proper price for certain assets/risk and we are in a world with multiple equilibria (or simple some markets disappearing) and this changes the predictions of this very simple linear model. That is the point that Blanchard and Leigh do that Brad DeLong also disagrees with. I used to think that these scenarios where impossible in advanced economies but my view on financial markets and the possibility of multiple equilibria has changed substantially during the 2008-2013 crisis.

But is the real disagreement about financial markets or about the role of exchange rates as an adjustment mechanism during times of crisis? Let me argue that they are related. There is a divide between US and European economists when it comes to this debate. Even among those who come from similar ideological backgrounds and support similar models, I have found that US economists tend to put a larger weight on the benefits of flexible exchange rates. Europeans tend to be more skeptical. It might be because there is a bias (Europeans are "proud" of the Euro). But I think that there is also a belief that financial markets (and foreign exchange markets) are more imperfect than what the traditional model of flexible exchange rates suggest. Bubbles, mispricing of currencies, financial imperfections, animal spirits, multiple equibria all move you away from the theoretical benefits of flexible exchange rates.

Who is right? I have no disagreement with the logical arguments that Brad DeLong makes, but what would really make me change my mind is empirical evidence about the behavior of interest rates or exports or exchange rates during the crisis that supports those models (e.g. why did the depreciation of the british pound not have a larger effect on exports?). My latest post had been motivated by the results of Rose on the irrelevance of exchange rate regimes during the crisis. The results are interesting and suggest that exchange rates matter less than what we think. They are not definitive, there are always hypothesis that cannot be tested with the data we have but to me that's the only place to make progress in this debate, we need more and better empirical analysis.

[Update: Paul Krugman does not like my arguments either and he asks for a model. Fair point and I do not have one but I see my arguments as being consistent with models that others have written. Looking for one when I find more time. But my argument is mostly empirical: I cannot think of many countries where a sudden stop has led to an expansion. To be continued.]

Antonio Fatás

Brad DeLong wrote a post yesterday to show that sudden (capital) stops should not be a concern for countries that have their own currencies. Let me start with all the arguments where I do not have any disagreement:

- Taking about the possibility of a sudden stop in the UK or the US makes no sense. I agree. The comparison that some establish to argue that the "US is the next Greece" is idiotic.

- Countries with fixed exchange rates that have accumulated a large amount of debt denominated in foreign currency are more likely to be exposed to crisis caused by sudden stops. Correct.

Where we disagree is on whether sudden stops are relevant to other countries with flexible exchange rates. My argument was that in cases where countries have been running large current account deficit for years, a sudden stop of capital could be contractionary (i.e. cause a crisis). Brad DeLong is more optimistic and argues (using the IS-LM model) that, on the contrary, a sudden stop will be expansionary because the exchange rate depreciation will boost exports. The argument is correct within the context of that model but I think that the model is missing several ingredients.There is no one real interest rate in financial markets. You might fix this by adding some risk premium to the model (e.g. the interest rate in the investment equation has an extra term). As long as that extra term is constant it will look as if you can still generate an expansion by controlling the real interest rate but I think that in some cases markets just fail to even provide a proper price for certain assets/risk and we are in a world with multiple equilibria (or simple some markets disappearing) and this changes the predictions of this very simple linear model. That is the point that Blanchard and Leigh do that Brad DeLong also disagrees with. I used to think that these scenarios where impossible in advanced economies but my view on financial markets and the possibility of multiple equilibria has changed substantially during the 2008-2013 crisis.

But is the real disagreement about financial markets or about the role of exchange rates as an adjustment mechanism during times of crisis? Let me argue that they are related. There is a divide between US and European economists when it comes to this debate. Even among those who come from similar ideological backgrounds and support similar models, I have found that US economists tend to put a larger weight on the benefits of flexible exchange rates. Europeans tend to be more skeptical. It might be because there is a bias (Europeans are "proud" of the Euro). But I think that there is also a belief that financial markets (and foreign exchange markets) are more imperfect than what the traditional model of flexible exchange rates suggest. Bubbles, mispricing of currencies, financial imperfections, animal spirits, multiple equibria all move you away from the theoretical benefits of flexible exchange rates.

Who is right? I have no disagreement with the logical arguments that Brad DeLong makes, but what would really make me change my mind is empirical evidence about the behavior of interest rates or exports or exchange rates during the crisis that supports those models (e.g. why did the depreciation of the british pound not have a larger effect on exports?). My latest post had been motivated by the results of Rose on the irrelevance of exchange rate regimes during the crisis. The results are interesting and suggest that exchange rates matter less than what we think. They are not definitive, there are always hypothesis that cannot be tested with the data we have but to me that's the only place to make progress in this debate, we need more and better empirical analysis.

[Update: Paul Krugman does not like my arguments either and he asks for a model. Fair point and I do not have one but I see my arguments as being consistent with models that others have written. Looking for one when I find more time. But my argument is mostly empirical: I cannot think of many countries where a sudden stop has led to an expansion. To be continued.]

Antonio Fatás

Wednesday, October 23, 2013

Dealing with a sudden stop

My post yesterday on how the US economy would have performed if it was going through the crisis as a member of the Euro area was an attempt to explain that the perspective of a small Euro country with limited credibility can be very different from that of the US. Robert Waldmann at Angry Bear is surprised by the macroeconomic logic I use so let me clarify what I had in mind -- given that what I am saying is quite standard.

A country with a current account deficit must have a matching capital inflow to finance the excess of spending above its income (this is an accounting identity). During the financial crisis many European countries faced a sudden stop -- which is defined as a situation where international financial markets are not willing anymore to fund the current account deficit of a country. This is something that any textbook discusses although normally in the context of emerging markets [by the way, it is not easy to use the IS-LM model to deal with sudden stops given that the IS-LM model is not the best model to analyze current account imbalances and situations where there is no price at which capital will fund a current account deficit].

If capital inflows stop it means that the country cannot afford to run a current account deficit (unless the rest of the world is willing to hold more of your currency (which is in fact a capital inflow). To close a current account deficit you need to reduce imports. If there was a way to engineer a fall in imports, there would be no consequence to domestic demand and GDP. And if at the same time your currency is depreciating you could see an increase in exports and possibly in increase in activity. But there is no way to engineer a fall in imports to close the current account deficit. Some of these imports are part of the supply chain in the domestic production but, more importantly, when foreign capital stops coming in you simply get an aggregate fall in spending that will affect domestic demand and production. In other words, when individuals of corporations who were borrowing abroad stop getting credit, there will be a fall in demand that will affect both domestic and imported goods. I am not saying anything new here, this is the way we teach about sudden stops and that's why we have mechanisms to provide liquidity during these times (e.g. lending by IMF) to ensure that the adjustment in the current account does not come in a very sudden way. There is no way to get out of this by inflation. Inflation can help dealing with monetizing internal debt (government debt) but cannot help smooth the consequences of sudden stop of capital that was financing a current account deficit. An exchange rate depreciation can help by increasing exports but this effect cannot be fast enough.

Before the crisis the US looked very similar to some of the Euro periphery countries (asset price bubbles, fast credit growth, large current account deficit,...). When the crisis started, the US managed to survived much better than Greece or Spain or Ireland. The point of my blog post was that the main reason for that is that the US maintained access to capital inflows (if any there was an increase in the desire of foreign investors to out their money in the US). The exchange rate itself did not help much, in fact the US dollar appreciated because of the capital inflows. And for Euro countries, the real problem was the large swing in capital flows from excessive inflows to a sudden stop. Competitiveness and the exchange rate played a much smaller role. That is my assessment after looking at the data. I think most economists agree with the existence of both effects but we seem to disagree with the relative importance of each of them.

[Update: I have written one more post that explains more of the logic behind my arguments.]

Antonio Fatás

A country with a current account deficit must have a matching capital inflow to finance the excess of spending above its income (this is an accounting identity). During the financial crisis many European countries faced a sudden stop -- which is defined as a situation where international financial markets are not willing anymore to fund the current account deficit of a country. This is something that any textbook discusses although normally in the context of emerging markets [by the way, it is not easy to use the IS-LM model to deal with sudden stops given that the IS-LM model is not the best model to analyze current account imbalances and situations where there is no price at which capital will fund a current account deficit].

If capital inflows stop it means that the country cannot afford to run a current account deficit (unless the rest of the world is willing to hold more of your currency (which is in fact a capital inflow). To close a current account deficit you need to reduce imports. If there was a way to engineer a fall in imports, there would be no consequence to domestic demand and GDP. And if at the same time your currency is depreciating you could see an increase in exports and possibly in increase in activity. But there is no way to engineer a fall in imports to close the current account deficit. Some of these imports are part of the supply chain in the domestic production but, more importantly, when foreign capital stops coming in you simply get an aggregate fall in spending that will affect domestic demand and production. In other words, when individuals of corporations who were borrowing abroad stop getting credit, there will be a fall in demand that will affect both domestic and imported goods. I am not saying anything new here, this is the way we teach about sudden stops and that's why we have mechanisms to provide liquidity during these times (e.g. lending by IMF) to ensure that the adjustment in the current account does not come in a very sudden way. There is no way to get out of this by inflation. Inflation can help dealing with monetizing internal debt (government debt) but cannot help smooth the consequences of sudden stop of capital that was financing a current account deficit. An exchange rate depreciation can help by increasing exports but this effect cannot be fast enough.

Before the crisis the US looked very similar to some of the Euro periphery countries (asset price bubbles, fast credit growth, large current account deficit,...). When the crisis started, the US managed to survived much better than Greece or Spain or Ireland. The point of my blog post was that the main reason for that is that the US maintained access to capital inflows (if any there was an increase in the desire of foreign investors to out their money in the US). The exchange rate itself did not help much, in fact the US dollar appreciated because of the capital inflows. And for Euro countries, the real problem was the large swing in capital flows from excessive inflows to a sudden stop. Competitiveness and the exchange rate played a much smaller role. That is my assessment after looking at the data. I think most economists agree with the existence of both effects but we seem to disagree with the relative importance of each of them.

[Update: I have written one more post that explains more of the logic behind my arguments.]

Antonio Fatás

Ben Bernankepoulos

Paul Krugman responds to my earlier post about how exchange rate regimes do not matter much (I was referring the work of Andrew Rose). Krugman has a different view on the issue and argues that countries in the Euro area have suffered from not having their own currency and this is visible by the higher interest rates that they faced relative to other countries. He makes a good point and the data speaks in favor of his hypothesis. I also think that Euro countries have suffered from being part of the Euro area because of many other reasons (e.g. they ended up adopting the wrong policy mix). Where I am less sure is about how much the ability to control the exchange rate mattered relative to other factors.

The only way to understand these effects would be to build a counterfactual: what would life without the Euro have looked like for these countries? I have tried to answer this question before and it less clear than what some might think. As an example, for those who see the current levels of unemployment in Spain as an example of the negative effects of not having your own currency, it is important to remember that job creation or unemployment in Spain look substantially worse when Spain had its currency (1980-1999) than since Spain has been a member of the Euro (1999-2013).

Let's build other counterfactuals just for fun: first, what if US economy had been a member of the Euro and, second, let's have Ben Bernanke running the central bank of a hypothetical Euro country that decides to leave the Euro area or did not even bothered joining the Euro (say Greece, that's the origin of the not-so-smart title for this blog post).

1. US as a member of the Euro area.

Let's start with the US economy being part of the Euro area. Of course we need some assumptions about the role that the US would be playing in this enlarged version of the Euro area. Imagine the US played a similar role to a small country in the periphery (Greece, Ireland or Spain). The ECB is still in Frankfurt and run by the German central bank ideology. Prior to the crisis it is very likely that the US would have seen an even larger inflow of capital from other European countries because there would be no exchange rate risk within the Euro area. So, for example, institutional investors or financial institutions in Germany would have invested even more of their portfolios in the US given that there would be no exchange rate involved (in some cases regulations limit the amount of exchange rate risk for these institutions). It is possible that this would have made asset prices in the US increase even further than what they did in the run up to the crisis and possible have the US run an even larger current account deficit. In other words, the imbalances that led to the crisis would have possibly been much larger.

Once the crisis started, there would be no room for depreciation of the exchange rate but if one looks at the data, the US dollar did NOT depreciate when the crisis started. The other way around, it appreciated relative to the Euro and other currencies.

It is very difficult to know what the Euro would have done if the US had been a member of the area, it is likely that it would have appreciated relative to other countries (because there would be no USD), but what seems plausible is that relative to the actual data the US would have seen a lower loss of competitiveness if it did not have its own currency (not sure how much that would have mattered but just trying to get some facts right). So this could have been good news for the US [This is coming from the fact that when your have your own currency some times it moves in the opposite direction than what you would like].

What about interest rates? Given the strength of the US economy one would have not expected the US becoming part of the periphery so interest rates would have remained low (as in Germany). But clearly, the large current account deficits that would have preceded the crisis could have put more pressure on the US than on a country like Germany that had large surpluses. The potential negative effect for the US would have been that membership in the Euro area would have made the pre-crisis imbalances worse possibly leading to more risk in terms of funding when the crisis started. This is my reading of what has happened in the Euro periphery: one the biggest cost of the Euro membership was the bubbles that the Euro facilitated in the years before, not so much the inability to adjust via exchange rates after the crisis exploded.

2. Ben Bernankepoulos.

Here is my second scenario: let's have a Euro periphery country leave the Euro (or never join) and have monetary policy follow the policies that Ben Bernanke has followed in the US (bring interest rates down to zero, aggressive quantitative easing). The ECB has already followed some of these policies so there will be some similarities but the fact that now this country would be managing its own currency would bring some additional effects. The currency would likely depreciate and that should help exports. How much is less obvious. The effects of exchange rates on exports or the trade balance is not easy to measure - as a comparison during the crisis the UK saw its currency depreciate relative to the Euro but the performance of exports was clearly weaker than that of similar countries such as Spain that did not have their currency.

And what would happen to capital flows? It is likely that capital will flow out of the country, given that the country started with a current account deficit this would be a problem (dealing with a sudden stop is never easy). If debt is denominated in foreign currency the situation could be dramatic (as in the Asian crisis in the 90s). But even if debt is denominated in local currency there is still an issue: there is the need to finance a current account deficit and in the absence of capital inflows it would lead to a collapse of internal demand. Yes, exports might be increasing but it is hard to see that this adjustment would be fast enough to compensate for the immediate correction required given the lack of funding. Unless the rest of the world is happy holding more of our currency, in which case we can finance our expenditures via monetary expansion. But for Euro periphery countries their credibility of their currency is of course not where the US dollar is. A sudden stop would require liquidity from external sources (IMF or other governments) to avoid an economic collapse. Not too different from what Euro periphery countries had to deal with as members of the Euro area -- except that as members of the Euro area they had more negotiating power because the other countries (e.g. Germany) were really scared of the idea of a break up of the Euro area.

The message from these two scenarios is that we are dealing with a complex question where there are potentially many effects going in different directions. No doubt that the policies that Euro countries have adopted during the crisis have very likely exacerbated the negative effects of the crisis (in particular the slow reaction of monetary policy and the contractionary nature of fiscal policy). But if any of these countries had been outside of the Euro area they would have struggled with other issues and the outcome might not have been too different. The biggest benefit I see of having stayed out of the Euro area is that the capital flows that fed the pre-crisis bubble would have probably been smaller and maybe made the crisis more manageable.

So the US, the UK or Japan offer some interesting lessons to Euro countries about the virtues of being able to manage your own currency and monetary policy during the crisis. But I think that those lessons are not easily applicable. Not every country has the credibility of the US or the UK to maintain capital flows during and after the crisis allowing for a slow adjustment in the current account. Japan starts with a current account surplus and a very strong home bias when it comes to the funding of the large government debt so the notion of a sudden stop does not apply. So currency regimes matter in significant ways but the effects go in different directions and measuring the net effect is not easy. In addition, this effect can be very different for different countries or periods so it is hard to generalize. The paper by Rose provides a way to measure these effects by analyzing a large sample of countries and shows that there are no significant differences in performance across different exchange rate regimes. It is a good starting point of a debate that is complex and likely to continue over the coming years (or decades).

Antonio Fatás

The only way to understand these effects would be to build a counterfactual: what would life without the Euro have looked like for these countries? I have tried to answer this question before and it less clear than what some might think. As an example, for those who see the current levels of unemployment in Spain as an example of the negative effects of not having your own currency, it is important to remember that job creation or unemployment in Spain look substantially worse when Spain had its currency (1980-1999) than since Spain has been a member of the Euro (1999-2013).

Let's build other counterfactuals just for fun: first, what if US economy had been a member of the Euro and, second, let's have Ben Bernanke running the central bank of a hypothetical Euro country that decides to leave the Euro area or did not even bothered joining the Euro (say Greece, that's the origin of the not-so-smart title for this blog post).

1. US as a member of the Euro area.

Let's start with the US economy being part of the Euro area. Of course we need some assumptions about the role that the US would be playing in this enlarged version of the Euro area. Imagine the US played a similar role to a small country in the periphery (Greece, Ireland or Spain). The ECB is still in Frankfurt and run by the German central bank ideology. Prior to the crisis it is very likely that the US would have seen an even larger inflow of capital from other European countries because there would be no exchange rate risk within the Euro area. So, for example, institutional investors or financial institutions in Germany would have invested even more of their portfolios in the US given that there would be no exchange rate involved (in some cases regulations limit the amount of exchange rate risk for these institutions). It is possible that this would have made asset prices in the US increase even further than what they did in the run up to the crisis and possible have the US run an even larger current account deficit. In other words, the imbalances that led to the crisis would have possibly been much larger.

Once the crisis started, there would be no room for depreciation of the exchange rate but if one looks at the data, the US dollar did NOT depreciate when the crisis started. The other way around, it appreciated relative to the Euro and other currencies.

It is very difficult to know what the Euro would have done if the US had been a member of the area, it is likely that it would have appreciated relative to other countries (because there would be no USD), but what seems plausible is that relative to the actual data the US would have seen a lower loss of competitiveness if it did not have its own currency (not sure how much that would have mattered but just trying to get some facts right). So this could have been good news for the US [This is coming from the fact that when your have your own currency some times it moves in the opposite direction than what you would like].

What about interest rates? Given the strength of the US economy one would have not expected the US becoming part of the periphery so interest rates would have remained low (as in Germany). But clearly, the large current account deficits that would have preceded the crisis could have put more pressure on the US than on a country like Germany that had large surpluses. The potential negative effect for the US would have been that membership in the Euro area would have made the pre-crisis imbalances worse possibly leading to more risk in terms of funding when the crisis started. This is my reading of what has happened in the Euro periphery: one the biggest cost of the Euro membership was the bubbles that the Euro facilitated in the years before, not so much the inability to adjust via exchange rates after the crisis exploded.

2. Ben Bernankepoulos.

Here is my second scenario: let's have a Euro periphery country leave the Euro (or never join) and have monetary policy follow the policies that Ben Bernanke has followed in the US (bring interest rates down to zero, aggressive quantitative easing). The ECB has already followed some of these policies so there will be some similarities but the fact that now this country would be managing its own currency would bring some additional effects. The currency would likely depreciate and that should help exports. How much is less obvious. The effects of exchange rates on exports or the trade balance is not easy to measure - as a comparison during the crisis the UK saw its currency depreciate relative to the Euro but the performance of exports was clearly weaker than that of similar countries such as Spain that did not have their currency.

And what would happen to capital flows? It is likely that capital will flow out of the country, given that the country started with a current account deficit this would be a problem (dealing with a sudden stop is never easy). If debt is denominated in foreign currency the situation could be dramatic (as in the Asian crisis in the 90s). But even if debt is denominated in local currency there is still an issue: there is the need to finance a current account deficit and in the absence of capital inflows it would lead to a collapse of internal demand. Yes, exports might be increasing but it is hard to see that this adjustment would be fast enough to compensate for the immediate correction required given the lack of funding. Unless the rest of the world is happy holding more of our currency, in which case we can finance our expenditures via monetary expansion. But for Euro periphery countries their credibility of their currency is of course not where the US dollar is. A sudden stop would require liquidity from external sources (IMF or other governments) to avoid an economic collapse. Not too different from what Euro periphery countries had to deal with as members of the Euro area -- except that as members of the Euro area they had more negotiating power because the other countries (e.g. Germany) were really scared of the idea of a break up of the Euro area.

The message from these two scenarios is that we are dealing with a complex question where there are potentially many effects going in different directions. No doubt that the policies that Euro countries have adopted during the crisis have very likely exacerbated the negative effects of the crisis (in particular the slow reaction of monetary policy and the contractionary nature of fiscal policy). But if any of these countries had been outside of the Euro area they would have struggled with other issues and the outcome might not have been too different. The biggest benefit I see of having stayed out of the Euro area is that the capital flows that fed the pre-crisis bubble would have probably been smaller and maybe made the crisis more manageable.

So the US, the UK or Japan offer some interesting lessons to Euro countries about the virtues of being able to manage your own currency and monetary policy during the crisis. But I think that those lessons are not easily applicable. Not every country has the credibility of the US or the UK to maintain capital flows during and after the crisis allowing for a slow adjustment in the current account. Japan starts with a current account surplus and a very strong home bias when it comes to the funding of the large government debt so the notion of a sudden stop does not apply. So currency regimes matter in significant ways but the effects go in different directions and measuring the net effect is not easy. In addition, this effect can be very different for different countries or periods so it is hard to generalize. The paper by Rose provides a way to measure these effects by analyzing a large sample of countries and shows that there are no significant differences in performance across different exchange rate regimes. It is a good starting point of a debate that is complex and likely to continue over the coming years (or decades).

Antonio Fatás

Monday, October 21, 2013

The wrong reading of the money multiplier

Via Barry Ritholtz I read the analysis of Lacy Hunt about how recent Federal Reserve policies have been a failure to lift growth. I am somehow sympathetic to the argument that Quantitative Easing has had a limited effect on GDP growth -- although one has to be careful when analyzing the effectiveness of QE by comparing it to the alternative scenario (no QE at all) rather than simply measuring the observed GDP growth. But I find that the analysis of the article is not accurate when it come to the working of central bank reserves (and I have made a similar point before). Maybe it is a matter of semantics but the way the author analyzes the relationship between reserves and the money multiplier is not consistent with the conclusions reached about the lack of effectiveness of monetary policy actions.

Let me highlight two pieces of the analysis that I have difficulty understanding. First, there is the argument that increasing the amount of Reserves (deposits of commercial banks at the central bank) not only is not helpful but can be a source of speculation and bubbles. The actual quote from the article is:

"If reserves created by LSAP (Large Scale Asset Purchases) were spreading throughout the economy in the traditional manner, the money multiplier should be more stable. However, if those reserves were essentially funding speculative activity, the money would remain with the large banks and the money multiplier would fall. This is the current condition."

How can reserves be funding speculative activities if they remain in the balance sheet of the banks? Reserves represent an asset in the balance sheet of commercial banks. They have increased by having commercial banks selling other assets to the central bank. So the amount of "riskier" or "less liquid" assets must have decreased. The author suggests that what is going on is the following:

"(Banks) can allocate resources to their proprietary trading desks to engage in leveraged financial or commodity market speculation. By their very nature, these activities are potentially far more profitable but also much riskier. Therefore, when money is allocated to the riskier alternative in the face of limited bank capital, less money is available for traditional lending. This deprives the economy of the funds needed for economic growth, even though the banks may be able to temporarily improve their earnings by aggressive risk taking."